Issued Date:2023/10/26 Greenhouse Gas

Issued By:iST

When companies are crafting their ESG sustainability reports, they often face a series of complex issues, including the identification of emission sources and challenges related to data collection. How can these ESG report requirements be met to garner positive evaluations from various stakeholders and gain recognition from international brand manufacturers?

Green House Gas

Global climate change has become a crucial environmental concern on the international stage, with the primary culprits being the seven major greenhouse gases (GHG) responsible for causing the abnormal climate warming phenomenon. Many governments around the world have initiated policies to reduce greenhouse gas emissions. These policies include setting energy efficiency and emission standards, implementing regulations, imposing carbon taxes or energy taxes, emissions trading, and encouraging voluntary reductions by businesses. Therefore, conducting greenhouse gas inventories is instrumental for companies to meet ESG (Environmental, Social, and Governance) requirements.

However, when companies begin greenhouse gas inventories, they often face various challenges such as identifying emission sources, collecting data, quantifying emissions, and proposing improvement measures, making progress difficult.

In this episode of iST’s classroom, we will draw from iST’s rich experience in guiding various clients in recent years, including globally renowned contract manufacturers, semiconductor equipment manufacturers, IC design houses, optoelectronics companies, electronic component manufacturers, electronic system manufacturers, and traditional industries among domestic publicly listed companies. We will explain how to efficiently conduct ISO 14064-1 greenhouse gas inventories, Task Force on Climate-related Financial Disclosures (TCFD), and product carbon footprint measurements in line with ISO 14067 standards. These three critical areas aim to help companies meet ESG-related requirements and remain competitive in the international supply chain.

Greenhouse Gas

Greenhouse Gas

1. Greenhouse Gas Inventory: Conducting Organizational Greenhouse Gas Inventories According to ISO 14064-1

Greenhouse gases refer to gases that can absorb specific wavelengths of thermal infrared radiation emitted from the Earth’s surface, the atmosphere itself, or cloud layers. These gases allow sunlight to pass through the atmosphere but trap heat on the Earth’s surface, preventing it from escaping into the atmosphere. If these gases accumulate, they can lead to a phenomenon known as global warming. Greenhouse gases are categorized into seven types, including carbon dioxide (CO2)、methane (CH4), nitrous oxide(N2O), hydrofluorocarbons(HFCs), perfluorocarbons(PFCs), sulfur hexafluoride(SF6), and nitrogen trifluoride(NF3). The term ‘inventory’ is akin to the concept of a health check. Companies conduct inventories to identify emission hotspots and then use the results to drive relevant reduction efforts.

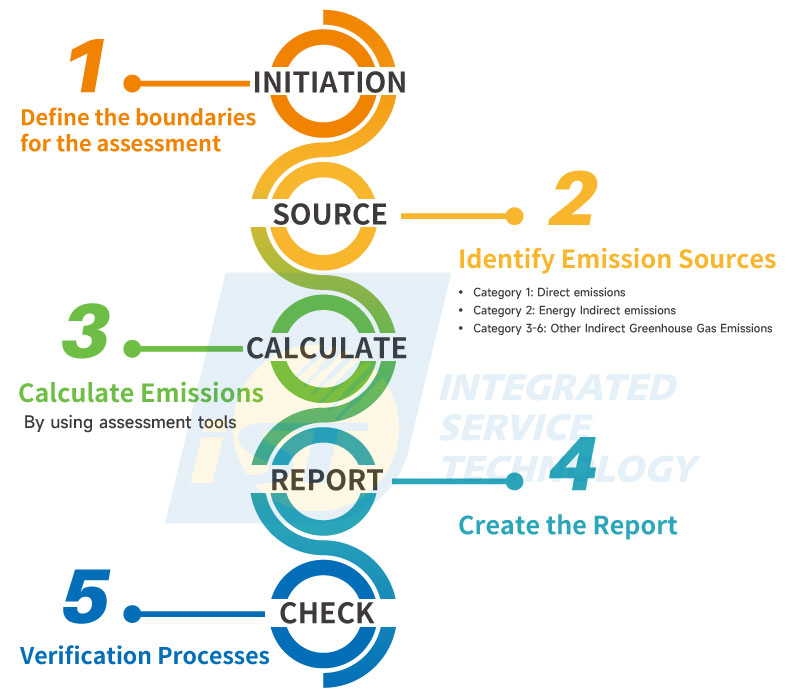

How should a company proceed with a greenhouse gas inventory? This process can be guided by the ‘ Initiation, Source, Calculate, Report, Check’ approach (as seen in Figure 1).

Figure 1: The five-word guide to implementing corporate greenhouse gas inventories.

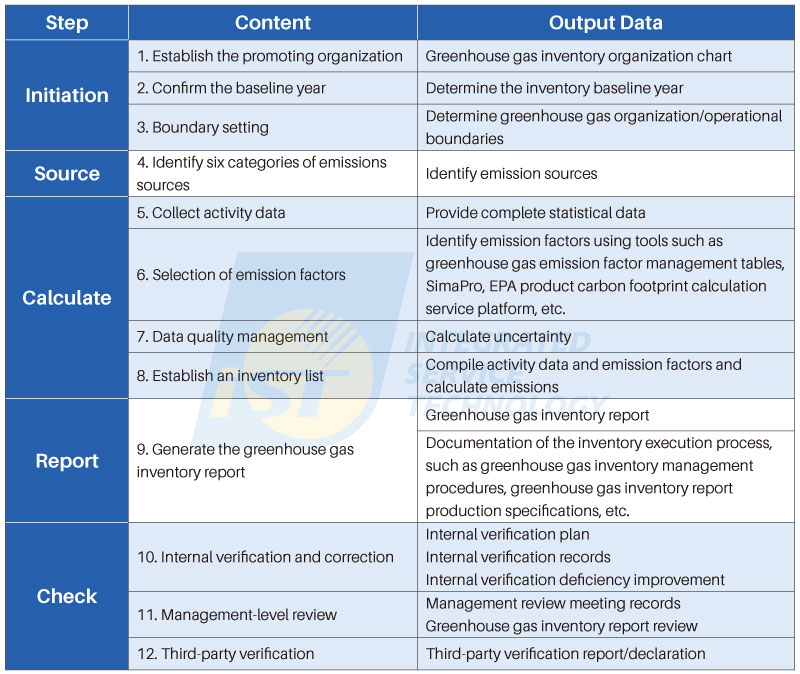

(Source: iST)Starting from the ‘ Initiation, Source, Calculate, Report, Check’ approach, the steps and data requirements for conducting an organizational greenhouse gas inventory for businesses are outlined in Table 1 for reference:

Table 1: Steps and data requirements for organizational greenhouse gas inventory in companies.

(Source: iST)

iST has found in its guidance process that clients often encounter two common challenges: ‘how to identify emission sources’ and ‘how to select emission factors and Global Warming Potential (GWP) values correctly.’ The following sections will provide clarification on each of these issues.

(1) How to Differentiate Different Emission Sources?

iST suggests that customers looking to implement a greenhouse gas inventory can identify emission sources within their organization through the following two methods:

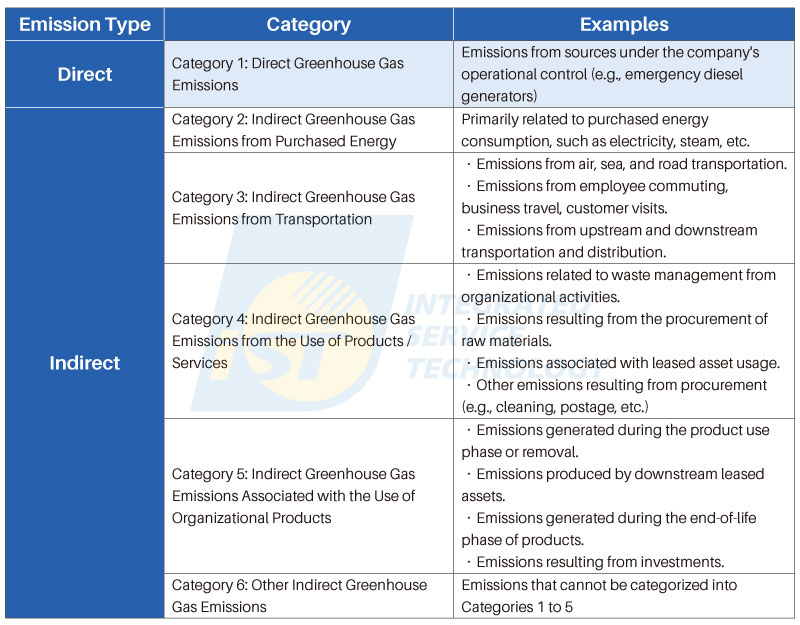

i. Identify emission sources according to ISO 14064-1, with examples of direct and indirect emissions (see Table 2).

Table 2: In ISO 14064-1, greenhouse gases are classified into six major categories based on direct or indirect emissions.

(Source: iST)

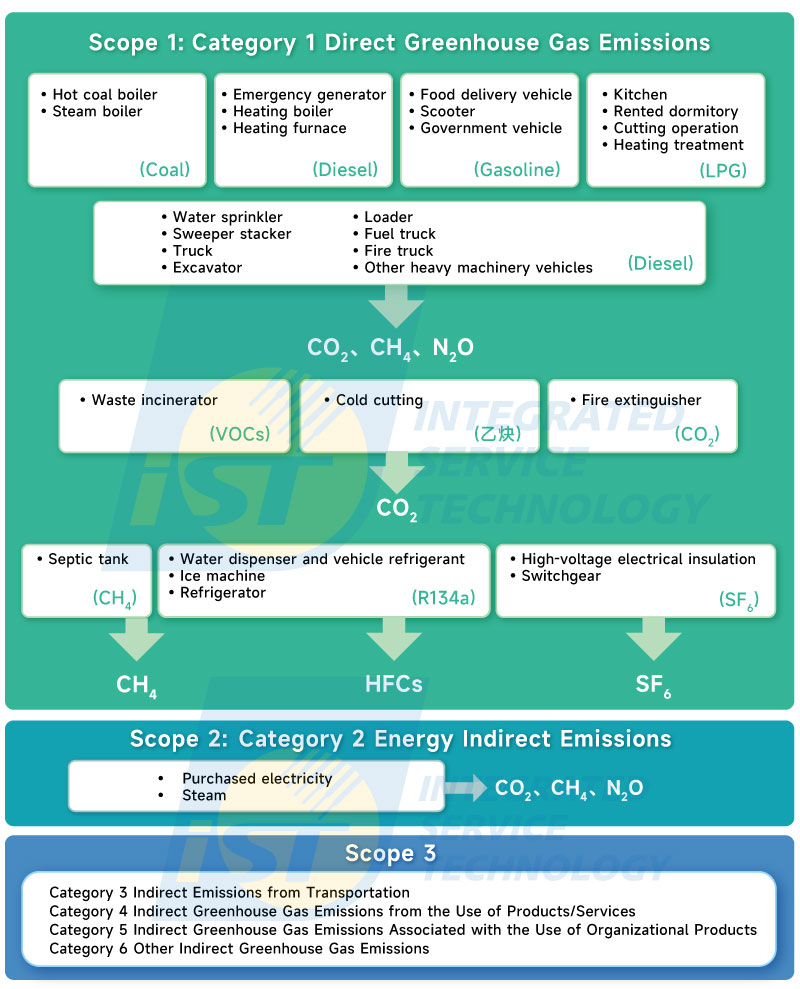

ii. Understanding Various Types of Emission Sources (See Figure 2).

Figure 2: This figure, also based on the classification of emission sources in ISO 14064-1, categorizes greenhouse gas emissions into three major categories. (Source: iST)

(2) How to Select Emission Factors and GWP Values Correctly

i. Emission Factors

iST recommends that you can sequentially discover emission factors through tools such as the Environmental Protection Administration (EPA)’s Greenhouse Gas Emission Factor Management Table, the Environmental Protection Administration’s Product Carbon Footprint Calculation Service Platform, and international software databases like SimaPro.ii. GWP (Global Warming Potential)

Global Warming Potential (GWP) calculates the impact of different greenhouse gases on warming by estimating conversion factors for their warming contributions, expressed in terms of carbon dioxide (CO2) equivalents. These standard conversion factors can be obtained from relevant announcements by the United Nations’ IPCC (Intergovernmental Panel on Climate Change). For more details, refer to this link.2. Introduction to Task Force on Climate-related Financial Disclosures (TCFD)

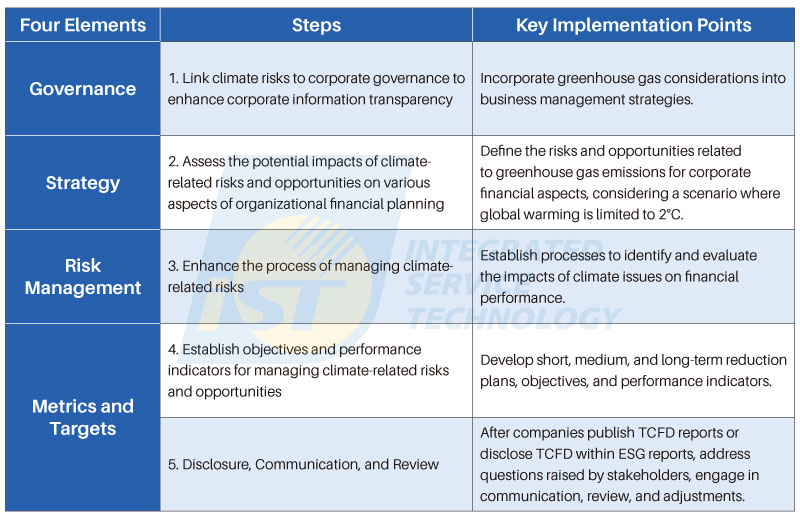

Given that climate-related impacts will affect a company’s operational costs and expenses, the Financial Stability Board (FSB) officially released consistent and voluntary recommendations, the Task Force on Climate-related Financial Disclosures (TCFD) in 2017. TCFD requires companies to disclose climate risks related to their business activities. After disclosing greenhouse gas emission information, companies can align with TCFD’s four pillars: ‘Governance,’ ‘Strategy,’ ‘Risk Management,’ and ‘Metrics and Targets.’

Currently, countries including Japan, the United Kingdom, New Zealand, the European Union, and Singapore, among others, mandate that climate-related disclosures by companies should align with TCFD. Taiwan’s financial regulatory authorities also require TCFD to be included in the content of ESG sustainability reports for publicly listed companies. This aids investors, financial institutions, businesses, and governments, among other stakeholders, in effectively assessing and determining which companies are well-prepared in the face of significant economic risks brought about by global warming.

Based on TCFD’s four pillars, the following are key points for implementing TCFD, as recommended by iST (see Table 3).

Table 3: Key TCFD Implementation Process as Recommended by iST(Source: iST)

3. Product Carbon Footprint

Product carbon footprint is a topic of great environmental concern, with both large and small companies actively exploring this issue. According to the relevant definitions in ISO 14067, the Carbon Footprint refers to the total greenhouse gas emissions generated by a product or service (e.g., e-commerce operations) over its lifecycle, expressed in terms of carbon dioxide equivalents per functional unit. When looking at the product lifecycle from a B2B perspective, it includes emissions from the raw materials stage to the manufacturing stage. From a B2C perspective, the lifecycle encompasses the raw materials stage, manufacturing stage, distribution and sales stage, usage stage, and disposal stage (including recycling and disposal), totaling emissions across five stages.

Figure 3: From a B2C perspective, the five major stages of the product or service lifecycle. (Source: iST)

Product Carbon Footprint (CFP) refers to the carbon emissions per functional unit of a product, such as one unit or one piece. Therefore, defining the inventory scope through methods like Product Category Rules (PCR) is crucial.

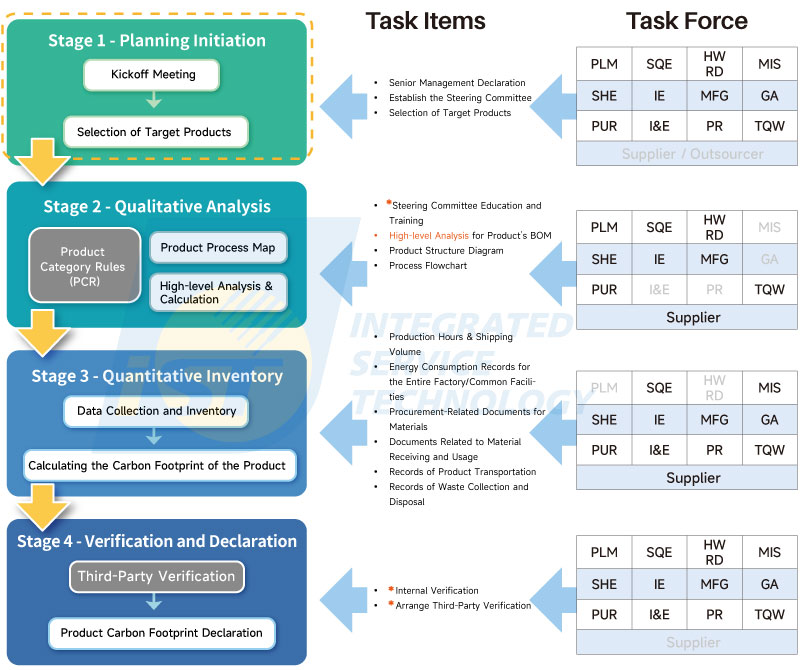

Figure 4: Product Carbon Footprint Implementation Process. (Source: iST)

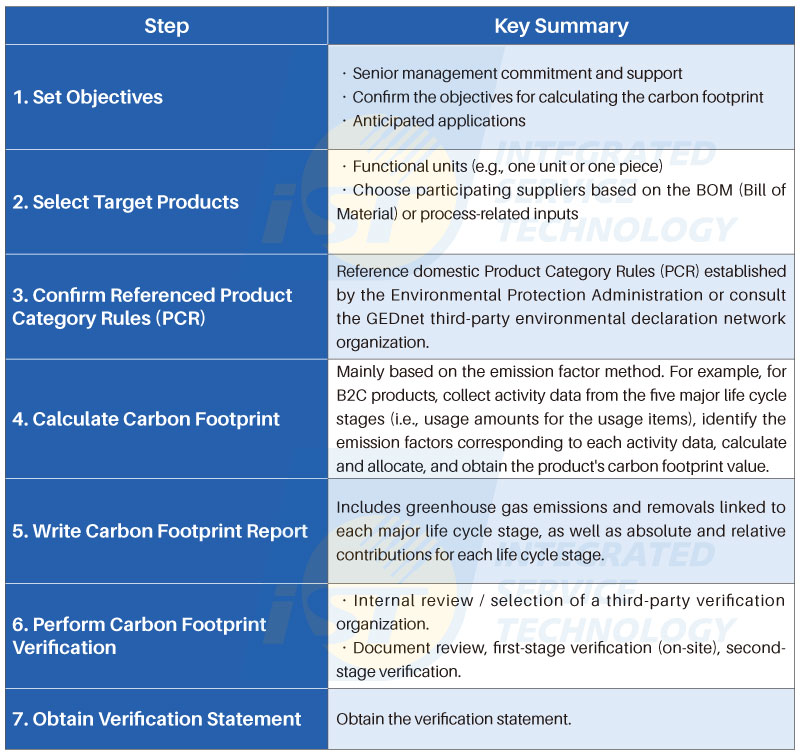

Regarding the implementation of Product Carbon Footprint, iST recommends that companies should primarily involve units including Environmental and Safety, Manufacturing, Plant Operations, Procurement/Supply Chain Management, and others. The following steps can be referenced to complete product carbon footprint verification and obtain a verification statement.

Table 4: Key points for product carbon footprint implementation. (Source: iST)

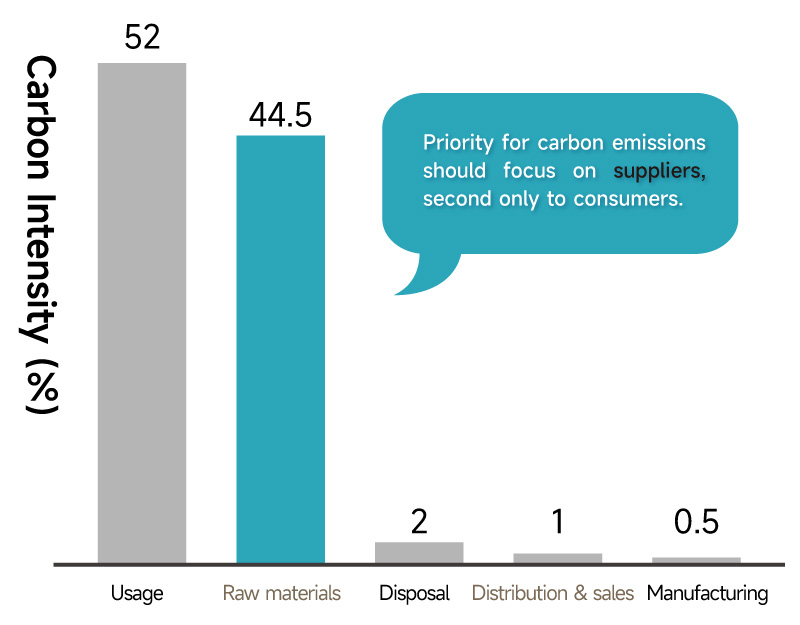

iST has gained extensive guidance experience since it initiated the Ministry of Economic Affairs’ Bureau of Energy’s technical project in 2011, titled ‘Product Carbon Footprint and Energy Conservation Carbon Reduction Information Service Platform and Tool Development Program.’ iST believes that for both B2C and B2B products, the supplier’s carbon emissions share and reduction opportunities are key aspects highlighting product environmental performance (see Figure 5). Effectively reducing overall product carbon emissions to enhance green product performance is one of the essential goals of implementing a carbon footprint. Therefore, on-site audits of suppliers are necessary, particularly for those with a significant emission contribution and local presence. iST defines approximately 40 supplier audit indicators, which companies can use to build a carbon reduction value chain in collaboration with relevant suppliers.

Figure 5: Looking at the carbon footprint generated in the five stages of a monitor’s lifecycle, starting with suppliers (raw materials) is a more feasible method for carbon reduction. (Source: An interview by Business Weekly with electronic assembly subcontractor Qisda in September 2023, 1870 issue of the magazine)

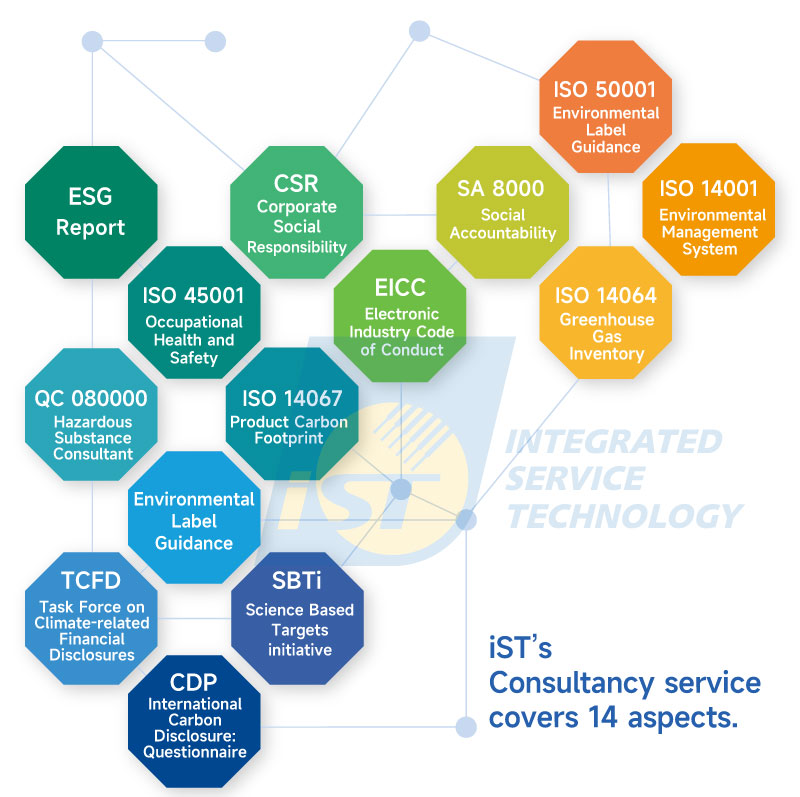

Leveraging its extensive experience in guiding over a hundred companies, iST has assisted clients in achieving various value-added certifications, enabling them to successfully enter the international industrial supply chain. In the past six years, among the 72 clients that iST has actively consulted, including globally renowned contract manufacturers, semiconductor equipment manufacturers, IC design firms, optoelectronics, electronic component manufacturers, electronic system manufacturers, and traditional industries among domestic publicly listed companies, all projects, except for seven that are still ongoing in 2023, have achieved a pass rate of 100%. In terms of ESG sustainability report guidance, iST can also assist with greenhouse gas inventories, product carbon footprints, recommendations for TCFD, Science-Based Targets initiative (SBTi), and ISO 50001 energy management and conservation services, among others (see Figure 6).

Figure 6: The 14 guidance areas that iST can assist companies with. (Source: iST)

In this article, we share our experience with all of you who have long supported iST. If you are interested in further details on greenhouse gas inventories and product carbon footprint guidance, please feel free to contact Mr. Lin at ext. 8807 or Ms. Hsu at ext. 8803 at +886-3-579-9909, or via email at web_isd@istgroup.com;marketing_tw@istgroup.com。